Betsson AB (BETS-B) - Mind the Valuation Gap

Betsson is a well-established Swedish online gambling company with a long and profitable record. The company has achieved a 10-year average FCF-margin of 23.5%, complemented by average returns on capital (ROIC, ROCE and ROE) exceeding 20% on a 3-, 5- and 10-year basis. With a robust balance sheet and net cash of approximately €53mm, Betsson is in a strong financial position.

CEO, Pontus Lindwall, owns approximately 1.1% of shares outstanding, equivalent to €13.9mm. Since these shares constitute a significant portion of his total net worth (similarly to several board members), there is a clear alignment between management and shareholders. In other words, both the board and management team have a clear incentive to maximize long-term shareholder value.

The global online gambling industry is expected to reach total revenues of €127.8B in 2028 (6.2% CAGR).

On a 12-month forward basis, Betsson is currently trading at 7x FCF and 7.5x normalized earnings, multiples that significantly undervalue the company’s quality and promising growth prospects in my opinion.

Business Model

Betsson AB was founded in 1963 with casino games, sports betting, poker and bingo as its core segments.

The business model can be described as a holding company with a portfolio consisting of popular brands including Betsafe, NordicBet and StarCasino. Additionally, the company has a B2B-segment for the sale of licenses and solutions to other gaming operators.

With FY23 revenues of €948.2m, Betsson is a leading online gaming company in Europe. Management has expressed an ambition of maintaining growth through a balanced combination of acquisitions and organic growth.

In 4Q23, Betsson held local gaming licenses in 23 countries spread between Europe, Africa, and North- and South America, an increase of 3 licenses compared to 4Q22.

Structure

The company structure results in the parent company being responsible for strategy and objectives, corporate governance and internal control, acquisitions and divestments, and financial communication.

The subsidiaries are responsible for the group’s operations, including platforms, gaming sites, technology and product development, brands, responsible gaming and regulatory compliance.

Revenue streams

Casino games is undoubtedly the largest segment, representing 72% of sales, while sportsbook and “other” constituted 27% and 1%, respectively.

Casino games’ FY23 share of sales has increased 600 basis points compared to FY22. The sportsbook segment’s sales fell 5.2% YoY, equivalent to a share decline of approximately 500 basis points. I should mention that the 2022 WC led to a significant short-term jump in activity for this segment, thereby creating difficult comps for 2023.

Other products (e.g., bingo and poker) still represented a miniscule share of sales, generating revenues of EUR 2.1m for FY23, representing 1% of total sales (2%).

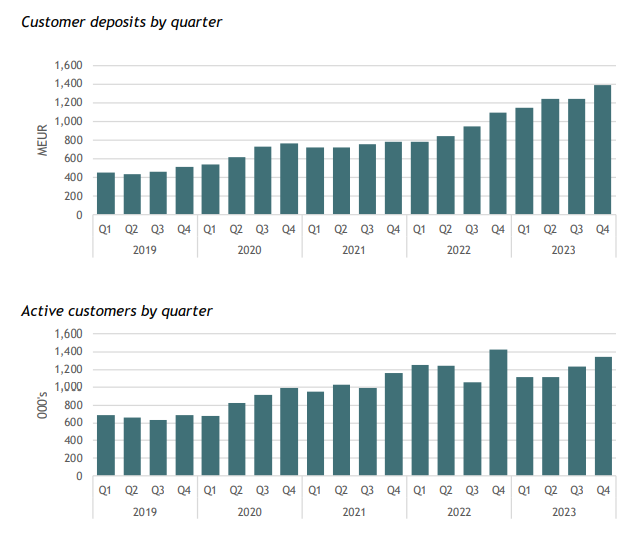

Customers and customer deposits

Active customers by quarter have approximately doubled during the last four years, from less than 700k customers in 1Q19, to exceeding 1.3m customers in 4Q23 (appr. 18% CAGR). The development has been somewhat volatile (partly due to a short-term surge in customers and customer deposits during the world cup), but the long-term trend is satisfactory.

Despite the number of active customers having experienced impressive growth, customer deposits have been the core value driver. Betsson has more than tripled customer deposits since 2019, from €400m in 1Q19 to roughly €1.4B in 4Q23.

This accomplishment has been achieved through a combination of organic growth, acquisitions and a diversified brand portfolio. Since the beginning of 2022, the top-line growth has also experienced a significant reacceleration.

Management and capital allocation

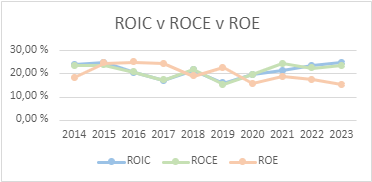

One of Betsson’s decidedly strongest sides is management’s impressive ability to allocate capital in an efficient and profitable manner. The average return on capital (measured in ROIC, ROCE and ROE) indicates that retaining earnings has been highly value-accretive for shareholders.

10-year averages:

Return on invested capital (ROIC) = 21.38%

Return on capital employed (ROCE) = 21.26%

Return on equity (ROE) = 20.17%

Both the chart and table below illustrate how the return on capital declined somewhat during the period 2013-2019, but also how these metrics have experienced a significant turn since 2020.

If you combine this with the company’s plan of expanding to the U.S. market (currently only B2B), it’ll be exciting to see whether this positive trend in return on capital persists.

An important test for management will be whether they remain disciplined enough to quickly end projects/initiatives and expansion to certain markets if they turn out to be value destructive. Growth solely for growths sake is never a rational argument.

Despite return on capital having been quite impressive historically, a positive spread between return on capital and the weighted average cost of capital is what determines whether current operations are value-accretive for shareholders. Luckily, return on invested capital has significantly exceeded the WACC, both on a 10-year-, 5-year- and 3-year average basis as illustrated in the table above.

Dividend policy

Additionally, Betsson has an attractive dividend policy, where management has expressed an ambition to distribute up to 50% of annual profits to shareholders. The dividend policy suggests two things:

(1) That management is shareholder oriented and wishes to distribute excess capital to shareholders instead of accumulating an unnecessarily large cash balance.

(2) That the company does not have enough attractive projects to justify retaining all earnings from a ROI perspective.

I prefer share repurchases to dividends, provided that this can be done at cheap prices – something I believe Betsson’s current valuation represents. Additionally, it’s a more tax-efficient method for distributing capital.

Betsson has strong free cash flow and a large cash balance. This is a two-edged sword. I would prefer management retaining all earnings given their impressive return on capital.

But at the same time such a situation could lead to “empire building”. Management could prioritize expansion and growth due to a desire of power and status, and not because they see highly value-accretive investment alternatives (think: Equinor’s USA-project that cost the company close to NOK 200B).

Alignment of interests

One of the most decisive factors to ensure the creation of long-term shareholder value is alignment of interest between management and shareholders. If the company does not have a clear incentive structure that ensures alignment between these interests, agency costs can occur.

This could result in the management (agent) making decisions to enrich themselves and maximize self-interest, rather than maximizing the values that accrue to owners/shareholders (principal).

Betsson’s roots go back to AB Restaurang Rouletter, founded by Bill Lindwall (the father of current CEO, Pontus Lindwall) and Rolf Lundström in 1963. In 1968 the company entered a partnership with Spelautomater to expand internationally.

Spelautomater was founded by Per Hamberg and Lars Kling, the latter today owning approximately 2.9% of Betsson. CEO Pontus Lindwall, and his mother, Berit Lindwall, own approximately 1.1% and 1.3% each.

Since these ownership interests constitute significant shares of their overall wealth, it’s reasonable to assume that both the management and board will make decisions in an attempt to maximize long-term shareholder value.

Recent financial results

In the 4Q23 report, Betsson revealed that Q4 marked the eight consecutive quarter with growth in both revenue and earnings.

Total group revenues amounted to €251.9mm (14% YoY), primarily driven by a strong increase in casino revenues (25%). Sportsbook, on the other hand, disappointed with a revenue decline of 5% YoY and margin contraction of 110 bps, from 7.3% to 6.2%.

Operating income delivered astounding growth, increasing from €40m to €57m (40% YoY), driven by margin expansion of 450 bps and higher sales.

Earnings grew 32% YoY, corresponding to earnings per share of €0.30 (€0.26). The substantial discrepancy in earnings growth and growth in eps was due to share dilution.

Given Betsson’s solid profitable operations, the significant balance sheet strength comes as no surprise.

With net cash of approximately €53mm, it will be interesting to see how the management team decides to allocate this cash balance (share repurchases, M&A, reducing debt, reinvestments or increasing dividends?).

At the end of 4Q23, Betsson had an equity ratio and debt-to-equity ratio of 0.63 and 0.58, respectively, combined with a highly attractive ICR of 13.40.

The number of active customers also grew satisfactory, with an increase of 10.7% QoQ. The fact that growth in both revenue and earnings exceeded the growth in quarterly active customers was due to several factors, including the significant growth in customer deposits and cost-cutting initiatives.

Valuation

Betsson is a quality business measured in both margins, return on capital and balance sheet strength. Since the company is approaching the maturity phase of its life cycle, a discounted cash flow analysis is a reasonable valuation technique.

I would still like to illustrate how unreasonably cheap Betsson currently is on a multiple basis relative to its profitability and underlying quality.

At the time of this writing, Betsson is trading at 6.6x FCF and 7x earnings on a trailing twelve-month basis. When adjusting for the company’s net cash position of approximately €53mm, the EV/FCFF and EV/EBIT multiples are 6.3 and 5.7, respectively.

To contextualize and clarify the irrationality behind these multiples, Betsson has reaccelerated its 3-year revenue CAGR to more than 17%, complemented by average EBIT-margins of ~ 20% and average returns on capital exceeding 20%.

Market

The global online gambling market is expected to reach total sales of €128.5B in 2028. This corresponds to a CAGR of 6.51%, and implies a market share of less than 0.1% for Betsson based on my revenue estimates for 2028.

In other words, the company can maintain a highly satisfactory growth rate without having to gain market share in a meaningful way. Additionally, I forecast revenue growth to revert towards a mean of 5% in 2028 and 2029, which one could argue is overly conservative.

Expanding into North America

As the pie chart below illustrates, RoW (“rest of world” - which includes North America in Betsson’s definition) constitutes an insignificant amount of current revenue.

The US online gambling market is expected to grow with an 8.7% CAGR between 2024-2029, resulting in a projected total revenue level of €32.8B in 2029.

Due to the promising North American market and strong growth projections, Betsson chose to launch a sportsbook-product under the Betsafe-brand in cooperation with Dostal Alley Casino in Colorado, in 2022.

At the end of 2022, sportsbooking was either legalized or awaited regulatory approval in 30 American states – suggesting that there are significant growth opportunities for Betsson in the US market.

Margins

In 2014, Betsson had an EBIT-margin of 16%. Since then, the margin has trended upwards, and reached 22.2% in 2023. With a 3-year average of 20.32% compared to the 5-year average of 19.19%, Betsson is showing glimpses of its profitability level during 2014-2015 (26.03% and 23.92%, respectively).

Despite Betsson likely increasing its marketing expenses in step with revenue growth, and licensing costs being significant, I expect them to experience margin expansion of 180 bps during the forecasting period. This equals an EBIT-margin of 24% in 2030, highly achievable given the satisfactory growth in customer deposits and managements plan of expanding/reposition into more profitable markets.

Capital expenditures

I also expect that further expansion into the RoW-segment (primarily investments in North America) and existing markets will result in a significant increase in annual capital expenditures (SEK 724mm in 2030 compared to SEK 465mm in 2023).

Shares outstanding

Next, I expect capital distributions to remain attractive, and being done through a combination of dividends and share repurchases (to exploit the current mispricing).

The model assumes an annual reduction of 0.25% in shares outstanding throughout the forecasting period. I decided to keep this reduction low in order to take potential dilution effects from management and board option exercises into account.

Terminal value

To compute the terminal value, I utilized the Gordon Growth formula, using a WACC and long-term growth rate of 9% and 1%, respectively. Consequently, these inputs resulted in a terminal multiple of 12.63, very reasonable given Betsson’s 10-year median multiples of 16.59x FCFE and 17.37x FCFF, respectively.

By discounting the terminal value and future cash flows on a per share basis with a discount rate of 15%, and adjusting for net cash, I get an intrinsic value per share of SEK 178.

This intrinsic value estimate implies that the current share price offers approximately 70% upside, equivalent to a MoS of 40%.

Despite the process of calculating a precise number for intrinsic value being quite ridiculous in itself, I consider the discrepancy between price and value sufficiently large enough to offer a high probability of delivering excess returns.

Risk factors

Regulatory risk is the most central risk factor for Betsson’s business. This includes regulations that make it difficult to maintain profitable operations due to high tax levels, and product- and marketing restrictions.

The company’s decision to withdraw their application for licensing in the Netherlands last year due to major delays in the approval-process is a good example of the difficulties and risks that arise due to regulations.

Betsson attempts to mitigate this risk factor through involvement in industrial bodies and active dialog with policy makers on different levels.

Payment process risk is also a factor that management currently considers increasing. Since Betsson is a global company, providing its services in several markets, there is consequently a need for multiple payment solution providers. This results in the rise of counterparty risk, risk of disruption and increased complexity, that may affect the company’s ability to quickly and efficiently execute deposits and withdrawals in gaming accounts.

Betsson operates in what is probably one of the most regulated industries globally, and therefore has to comply with several laws and regulations. The national and international regulatory environment is under constant change, and the bar for compliance within consumer protection (included responsible gaming, marketing and bonus offers), protection of privacy (GDPR), measures against money laundering/terrorist financing and anti-corruption is constantly increasing.

The lack of compliance of the aforementioned points can lead to fines and lawsuits, and consequently the weakening of the company’s reputation and earnings power.

Summary

Betsson is an exciting online gambling company well-positioned to capitalize on the significant growth-opportunity in North America. The company also possesses the necessary financial strength to enjoy the industry’s structural tailwinds.

With an average return on capital exceeding 20%, and which clearly exceeds the company’s cost of capital, retaining and reinvesting earnings into the business is value-accretive for shareholders. The company has also expressed an ambition of maintaining a dividend policy of 50% of all profits after tax.

Additionally, management and shareholders have a clear alignment of interest, given several insiders’ significant ownership relative to their total net worth.

Due to the aforementioned growth opportunities, impressive return on capital and capital allocation, and strongly aligned interests between management and shareholders, I consider the single digit multiples Betsson currently trades at as unreasonably low. The DCF also illustrated how the stock is still significantly undervalued despite using what I consider highly achievable assumptions.

I therefore believe that the downside risk is limited, and that we as shareholders can enjoy a dividend yield of 6-7% while we wait for the market to correct its mispricing.